For decades, Germany was synonymous with economic strength. Ever since World War II, it enjoyed the so-called «Wirtschaftswunder,» or economic miracle that followed the postwar recovery, which blessed Germany with almost four decades of high growth.

High growth thanks to German engineering, and manufacturing industries. The economic growth eventually slowed down, but Germany had established itself as the industrial heart of Europe, fueled by exports of products with large margins like cars machinery, and chemicals.

Companies like Volkswagen, BMW, Siemens, and BASF became global leaders with German products seen as pinnacles of quality and reliability. As a result of all that, people in Germany enjoyed high salaries, and high quality of life.

Their economic model was built on a few key pillars; strong manufacturing base. A highly skilled workforce, commitment to quality, and very strong exports. But this has come to an end. Last year, Germany was the only G-7 economy to shrink. It`s also the group`s slowest-growing economy with a growth to GDP at -0.1%.

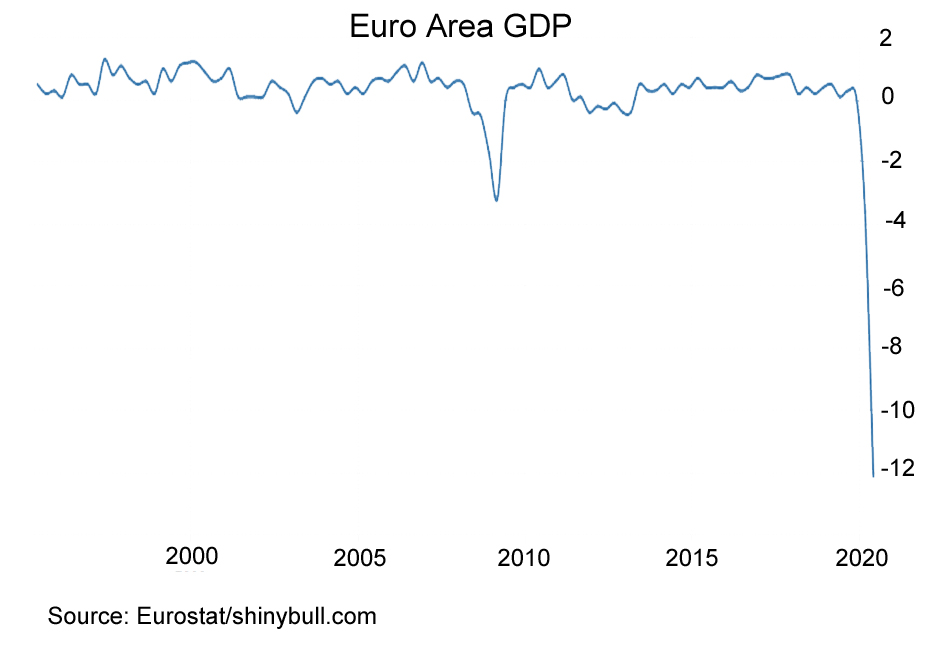

It goes up and down. Down -0,5, up 0,1, down, 0,1, up 0,2, down -0,4, up 0,2, and then down again to -0,1.

Picture: Old economy vs New economies

Germany, long considered the economic engine of Europe, is currently facing significant challenges, leading to concerns that its economy may be stalling or «broken.» What in the world is happening in Germany, and what are the key factors that are affecting their economy right now?

It`s an energy crisis. Germany was dependent on Russian Gas. Germany relied heavily on Russian natural gas before the war in Ukraine. The subsequent sanctions and supply disruptions have led to a severe energy crisis, pushing up prices and harming energy-intensive industries like chemicals, manufacturing, and heavy machinery.

They also have a green transition challenge. Germany is trying to transition to renewable energy, but the shift away from nuclear and coal has left the country vulnerable during this energy crunch. This has increased costs for businesses and households, causing slower growth.

Germany`s economy is heavily reliant on exports, especially in industries like automotive and machinery. Global demand has softened, and supply chain disruptions from the COVID-19 pandemic continue to affect production.

The German auto industry, in particular, has been slow to transition to electric vehicles compared to competitors like Tesla, and Chinese manufacturers. This lag is putting pressure on a key pillar of the country`s economy.

Germany`s economy narrowly avoided recession in early 2023, but growth remains sluggish. High inflation and low consumer spending have contributed to weak economic activity. The combination of rising wages, energy prices, and inflationary pressures has increased production costs, leading to reduced profitability for businesses.

On top of that, you have an aging population. Germany`s population is aging rapidly, and the working-age population is shrinking. This is leading to labor shortages in key sectors and higher social welfare costs, creating long-term economic challenges.

In addition; they have migration struggles. While the country has relied on immigration to fill gaps in the labor market, recent shifts in public sentiment and policy restrictions have made it harder to sustain this approach.

Their biggest companies have been there for about 100 years, but there is a shift in the market. Germany has been criticized for lagging behind in digitalization and innovation, particularly in fields like AI and tech start-ups. This is reducing its competitiveness in the global economy.

Another problem is Germany`s heavily regulated business environment and complex bureaucracy. This can stifle innovation and make it harder for new businesses to scale up.

Like many others, Germany has trade challenges and the global demand is weak. As the global economy faces uncertainty, especially with China`s slowing growth, demand for Germany`s exports has dropped.

Germany`s economic model has long been dependent on strong export markets, so this is a major issue!

At least; EU Tension. Economic divergence within the European Union, especially between northern, and southern European economies, adds another layer of complexity, affecting Germany`s trade relations within the bloc.

It all started in France. Yellow Vest protesters went to the streets for months and years and protested against higher oil prices, electricity bills, and expensive toll stations. Their standard of living was shrinking.

This happened at a time when Donald Trump was cutting taxes and made the best economy in the U.S. ever. People in France asked for a Trump-like figure, but everything has gone straight up since then, and now we see severe problems in Germany and other places.

Picture: Yellow Vest protesters against high oil prices and low standard of living

This is happening at a time were productivity in the U.S. is great. Germany`s productivity is down -0,1%, while the productivity in the U.S. is up 3%. They are the best. They are at the top of the list! Even better than China! And the stock market goes up. Wow!

Germany`s economy is not «broken,» but it is facing severe challenges. Energy costs, inflation, global demand weakness, and structural issues in key industries like manufacturing are causing slower growth.

Long-term concerns like demographic changes and lagging investment in innovation also threaten future competitiveness. While these challenges are significant, Germany has strong economic fundamentals and could recover with strategic reforms and investments.

However, the current climate is tough, and the country is at a critical point in addressing these issues. Germany is in trouble.

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Shinybull.com. The author has made every effort to ensure the accuracy of the information provided; however, neither Shinybull.com nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities, or other financial instruments. Shinybull.com and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.