China`s growth plummeted -6,8 YoY in Q1. The growth in the U.S is still on the right side, coming in at 0,3 percent YoY in Q1. But if you look at the quarter, the growth in China is down -9,8 percent, while the U.S growth is down -4,8 percent.

The annulized 4,8 percent drop in Q1 of 2020 markes the end of the longest period of expansion in America`s history. The drop is the steepest pace of contraction in GDP since the last quarter of 2008 (financial crisis).

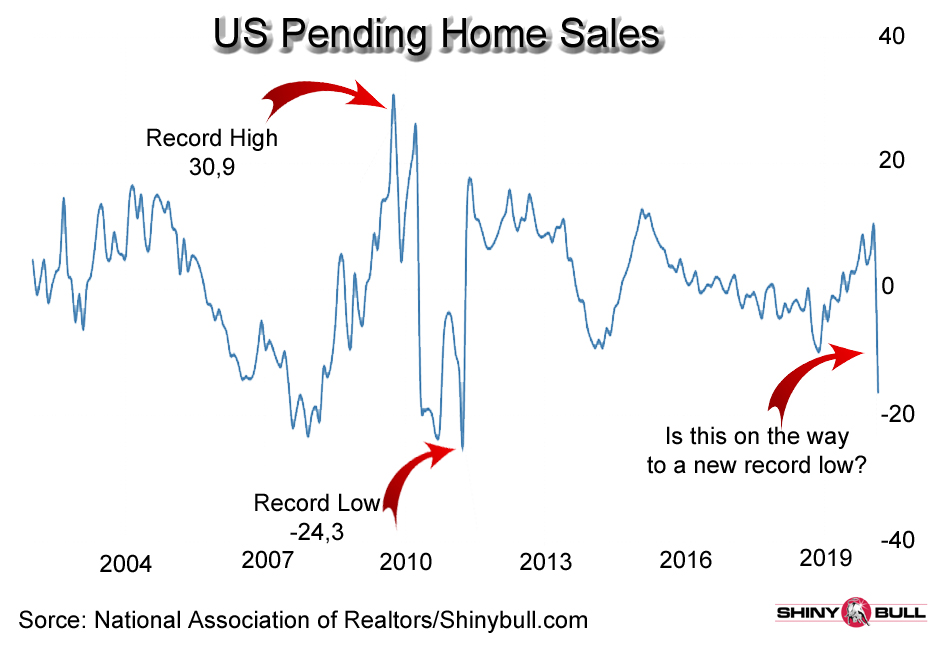

The Covid-19 pandemic forced several states to impose lockdown measures in mid-March and that pushed millions of people out of work. The unemployment rate go straight up while the pending home sales go straight down.

Contracts to buy previously owned homes in the US dropped 16,3 percent YoY earlier in March this year, and that is the biggest annual decline since April 2011, amid the Covid-19 crisis. On a monthly basis, pending home sales went down 20,8 percent, which is the largest drop since May 2010.

Unfortunately, it seems like this is just the beginning.

The next quarter can be very ugly, while the unemployment rate can go straight up to Great Depression levels. The growth in the US can plunge more than 30 percent. If that is happening, what do you thing will happen to the pending home sales?

The numbers are expected to get even worse in April as the government surveyed businesses and housholds for the report in mid-March, before majority of people was under some form of a lockdown.

Trump`s economic adviser Kevin Hassett said unemployment in the US can soar to 17 percent. In March the unemployment rate was 4,4 percent in the US.

During the financial crisis, the US lost about 9 million jobs, but now the US is losing that many jobs about every 10 days, Hassett told ABC on Sunday.

This is sad, because all the jobs created since the Great Recession (2008) have been wiped out. So far, we are talking about 26 million and it can be worse. Hassett told ABC the unemployment will surge to levels not seen since the Grat Depression (1929).

During the Great Depression, about 15 million jobs were lost.

So, we know what`s coming. People without job and money will not buy a house.

Pending home contracts generally are seen as a forward-looking indicator of the health of the housing market because they become sales one to two months later. This summer holiday will be very special.

To contact the author of this story: Ket Garden at post@shinybull.com

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Shiny bull. The author has made every effort to ensure accuracy of information provided; however, neither Shiny bull nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Shiny bull and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.