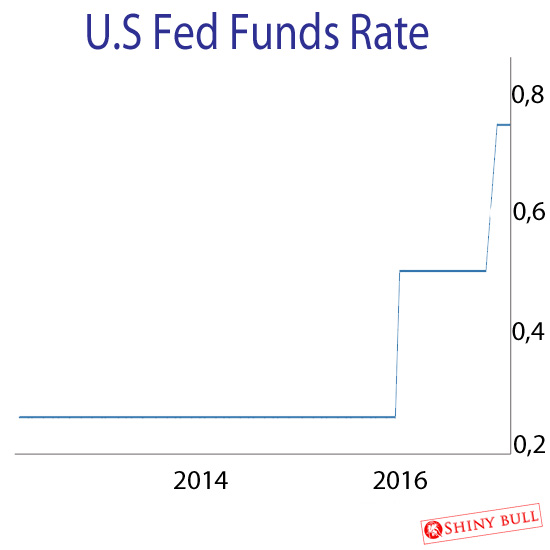

The stock market has been in a euphoric rally since Donald Trump won the election in November last year. This is something that Janet Yellen and the FED has monitored. Not only that. They also monitored strong economic data which have strengthened the case for a rate hike.

As you may know, the FED raised the rates a few days ago, and normally after a rate hike, the stock market drops. Thats the case right now, but the market didnt fall much. Janet Yellen said the FED will continue to raise the rates. What will happen then?

The FED came out with Scenarios for annual stress test required under the Dodd-Frank Act Stress Testing Rules and the Capital Plan Rule on February 10, 2017. It is just a forecast; an Armageddon forecast, which is called «Adverse Scenario» Report, and the scenarios are not forecasts of the FED.

The adverse and severely adverse scenarios describe hypothetical sets of conditions designed to assess the strength of banking organizations and their resilience to adverse economic environments. The baseline scenario follows a profile similar to the average projections from a survey of economic forecasters.

We must be prepared for higher long-term interest rates. What is that suppose to mean? First of all; that is good for banks with retail customers, simply because retail customers usually have checking accounts with zero interest on them.

So, if the rates rise, the spread in the banks rise simply because the banks will make more on their lending. About 2,000 banks has disappeared the last seven years, which means the competition among the rest is not that big anymore.

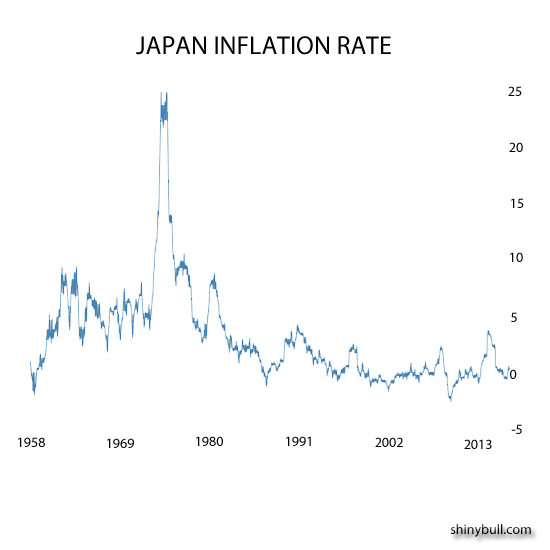

We can also see a steeper yield curve and regionally concentrated episodes of deflation. More pronounced in Japan, but less severe in the Euro zone and Asia and absent in the UK and US.

This is the major shifts we will see in the FED`s «Adverse Scenario» for 2017, and U.S banks will be stress-tested again. The apocalyptic scenario means that the level of U.S real GDP will decline in the first quarter of this year.

The US economy advanced an annualized 1,9 percent on quarter in the three months of 2016, slowing from a 3,5 percent growth in the previous period and matching earlier estimates. Consumer spending rose faster than anticipated while business investment was revised lower. Last year, the GDP expanded 1,6 percent, which is the lowest since 2011.

Check out next GDP number at 2017-03-30 at 12:30 PM.

In the scenario, the unemployment rate increases to 10 percent, by the third quarter of 2018, and short-term treasury rates fall and remain near zero. House prices will also decline by about 25 – 35 percent, through the first quarter of 2019, and so will equity prices.

In the same scenario, we will se a slowdown in Asia, severe recessions and the dollar will appreciate against euro, the pound sterling and the currencies of developing Asia.

I think the next big think to look at now is the election in France. If Le Pen and the populist wins, it can turn things upside down, and start a new international crisis. Until then, trade in small caps are profitable when rates rise, and higher rates doesn`t stop tech stocks like Alphabet, Apple and Amazon from surging. This is the bull market that everyone hates.

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Shiny bull. The author has made every effort to ensure accuracy of information provided; however, neither Shiny bull nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Shiny bull and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.