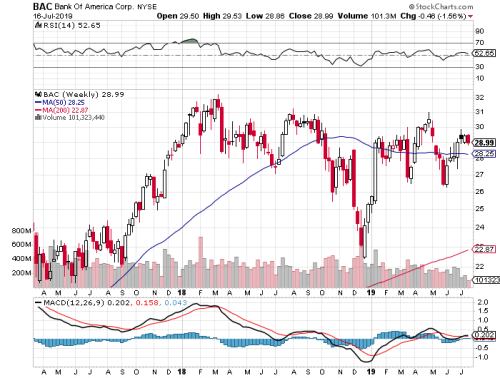

Bank of America peaked in October 2006 at $54, and started to decline after that. It plummeted during the financial crisis and you had the chance to buy the stock below $4 in early 2009. That feels like a «bank robbery». What now as the price is $13,27?

Buying Bank of America at about $4 is ridiculously cheap, but $13,27 is still cheap. This can be a big scoop for value investors as Bank of America is paying a great annual dividend. The financial crisis reduced its dividend to only $0,01 per share, but later increased to $0,05 in 2014.

The bank`s yield comes in a solid third place among its competitors like JPMorgan Chase, Wells Fargo and Citygroup. The shares are trading well below its book value and they allocated $4 billion on share buybacks compared to about $2 billion for dividend payments.

Warren Buffett bought $5 billion worth of shares in Bank of America in 2011. Many investors were skeptical about that decision because the bank had adopted a ton of risky loans when it bought Merrill Lynch and Countrywide Financial. It was very risky at that time. On top of that if was only three years after the financial crisis.

I bet Warren Buffett knew what he was doing; being greedy when others were fearful. Four years later, he doubled his money and on top of that he got six percent dividend for his preferred shares. Buffett and value investors will not the next bears I think, but there are many things to fear.

Chinas slowing growth can be a reason to dump the stock. So can possible a «Brexit». Bank of America is warning its managers to not use the word «Brexit» when they talk to their customers. They doesnt want to support one side or the other in the all-important June 23 vote.

Bank of America has plummeted more than 20% so far in 2016, and remain in the worst position of the retail banks. The bank topped its earnings expectations in Q4 and managed to miss revenue expectations by about $500 million.

The trend is not good for the bank and this trend is expected to continue as they has forecasted further weakness in its trading and investment banking revenue. Projected YoY declines in these segments outpace the losses of its peers.

The energy sector along with increased expenses and larger capital deployment will hamper the banks earnings this quarter.

Many large banks have large loan exposure to risky assets in the oil & Gas industry. 3,8% of total outstanding loans, or $21,8 billion is related to energy loans in Bank of America. In comparison, JPMorgan has 6% of total outstanding loans, or $42,1 billion.

Energy borrowers announced draws of more than $3 billion in Q1. What will Bank of America say about that and what is the banks next step in the energy sector?

Estimize expect an earnings per share of $0,25, which is two cents higher than Wall Street, on $20,87 billion in revenue, about $28 million ahead of the sell-side. Estimates have been feverishly cut ahead of its earnings, falling 18% in the past 3 months.

That said, Bank of America is still projecting favorable YoY growth of 4% on the bottom line.

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Shiny bull. The author has made every effort to ensure accuracy of information provided; however, neither Shiny bull nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Shiny bull and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.