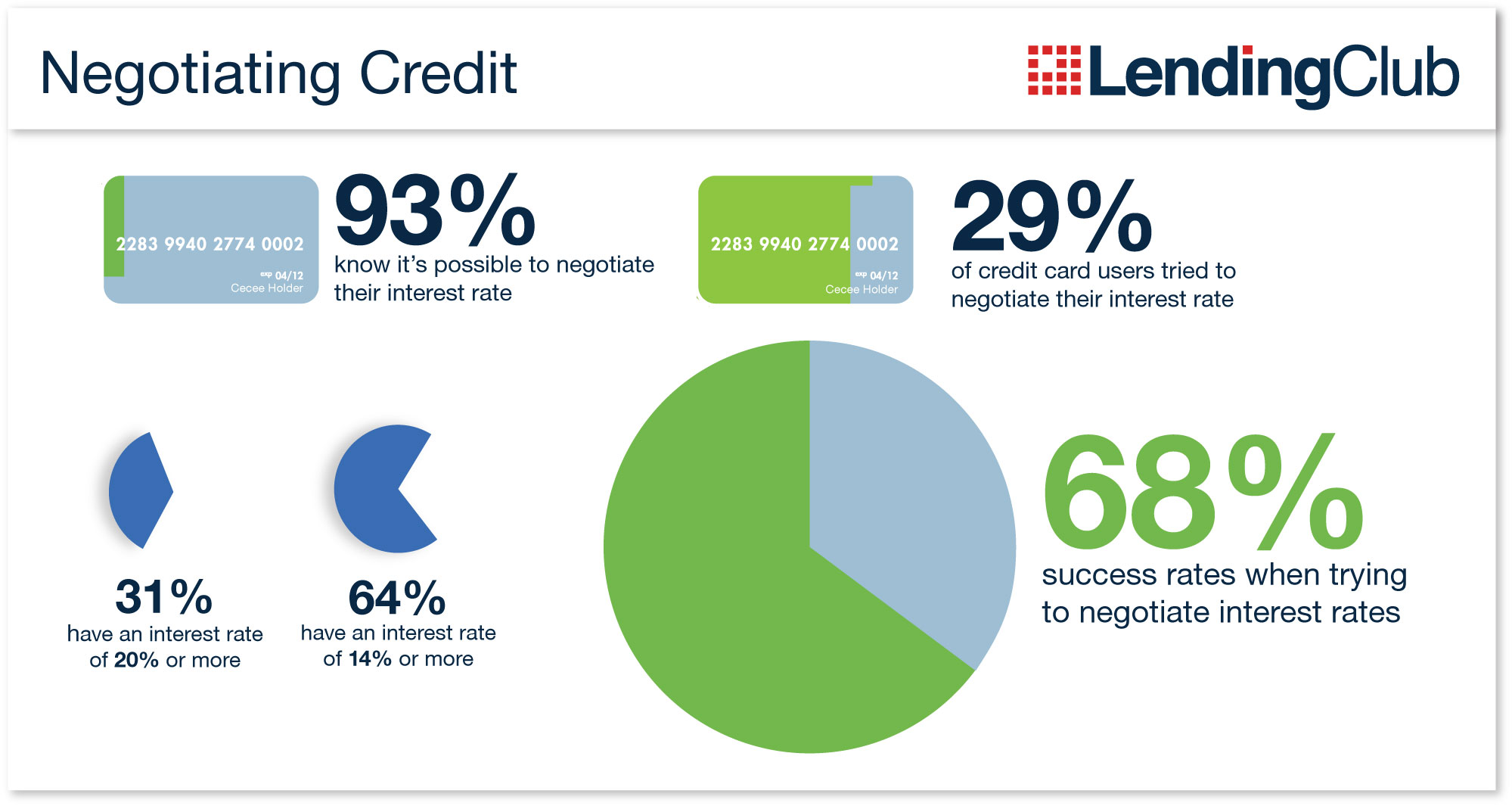

It is ok to have a credit card, but sometimes it can be very expensive. That is not ok for you, but it is big business for your bank. They will earn a lot of money on you. But what if I say that you can cut your credit card rate by several percentage points?

If you have too much money, what if I say that you can earn 8% on your cash? You are not stupid, so you wouldn`t say no to that. You would be interested in borrowing, but you would be interested in earning an 8% rate on your cash too. You will earn no matter what you do. How is that possible?

It`s possible because of the new system called peer-to-peer (P2P) lending.

This is a new platform where borrowers meets lenders with the aim of cutting out banks entirely. It`s more like debt-based crowdfunding, and one of the companies in this business went on the stock exchange at the same time when Alibaba entered the IPO market.

When everybody talked about the Alibaba IPO, nobody talked about the new IPO in the P2P lending market. LendingClub Corporation (LC) entered the market in 2014 and are the world`s largest P2P lending marketplace.

This is a company that started in 2007 and their loan origination have totaled over $7,6 billion from 2007 to 2014. They are small, but they are growing fast, and more P2P lending companies can enter the scene.

Their business model is simple. Lenders receive 13% and after deducting 1% for fees and adjusting for a 4% annual default rate, it`s 8% left to the investor. You will win as an investor, but as a borrower, you will too, because they are competitive to other banks.

Without a doubt, this is a threat to the traditional banking model.

This is a threat to traditional Credit Card Cartel like JPMorgan Chase, Bank of America, American Express, Capital One, U.S Bancorp, Discover and Citigroup. They account for about three-quarters of U.S credit card transactions, so consumer lending is big business.

The financial institutions will try to infiltrate the market.

Santander Consumer USA purchased 25% of LendingClub`s total origination for a term of three years in 2013, and LendingClub have seen a growing influx of capital from institutional investors who have begun to dominate the industry.

That`s hedge funds, asset managers, pension funds and family offices to name a few. An analytics firm called Orchard Platform, that caters directly to institutional investors can help them deploy capital at scale via lending platforms.

The shares of LendingClub Corp rose +4,21% today after announcing partnership with Citigroup Inc and Varadero Capital. What will the bank regulators say to that kind of partnership if this is the trend? Will they require that LendingClub have more of its own capital at risk?

LendingClub will work with Citigroup to provide as much as $150 million in affordable loans to underserved borrowers. The loans will be issued by WebBank, based in Utah, and purchased by Varadero Capital via a credit facility from New York-based Citigroup.

LendingClub and their competitor Prosper Marketplace Inc are leading a technology-driven push to lower borrowing costs, and that`s less than a decade after bad lending decisions led to a global credit crisis. I`m worried right now when I think of where we are in the credit cycle.

We need more competition in the banking sector and Lending clubs can do something with that.

What we see now is bank innovation. Probably a bank revolution.

Online credit marketplaces is the future.

Click the link below and check out the Fan Fund

https://www.eventbrite.com/e/fan-fund-tickets-15580655159

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Shiny bull. The author has made every effort to ensure accuracy of information provided; however, neither Shiny bull nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in precious metal products, commodities, securities or other financial instruments. Shiny bull and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.